What Are Medicare Prescription Drug Plans?

Medicare Part D is the federal prescription drug benefit program that helps Medicare enrollees cover a portion of the costs of prescription medications at participating pharmacies. It was first introduced under the Medicare Prescription Drug, Improvement, and Modernization Act of 2003.

Part D is optional, and beneficiaries must choose a plan offered by Medicare-approved private insurers.

Who Is Eligible?

Everyone with Original Medicare (Part A or Part B) is eligible to enroll in a Part D plan, regardless of health status or income.

If you have or enroll in a Medicare Advantage (MA / Part C) plan that includes drug coverage, that serves as your Part D benefit.

You must actively select a plan during an enrollment window to avoid lifetime penalties.

How PDP Plans Work (2025 Updates)

1. Benefit Structure & Stages

Starting January 1, 2025, the Part D benefit has been simplified into three stages:

Deductible stage (if your plan includes one)

Initial coverage stage

Catastrophic coverage stage

The old “coverage gap” or “donut hole” is effectively eliminated under new rules: beneficiaries will now receive continuous cost-sharing until they hit the catastrophic threshold.

2. $2,000 Out-of-Pocket Cap

One of the most significant reforms is a $2,000 annual cap on out-of-pocket prescription drug costs (for costs under Part D) as of 2025. Once you reach that limit, your plan must cover 100% of further drug costs for the remainder of the year (for covered drugs).

This cap is indexed and may increase in future years (e.g. projected $2,100 in 2026).

The average Part D premium in 2025 is approximately $46.50 monthly, lower than in prior years.

Plans may have deductibles, although many plans limit or eliminate them.

Cost-sharing (copays/coinsurance) applies until you reach the out-of-pocket cap.

4. Income-Related Monthly Adjustment Amount (IRMAA)

If your income (from two years prior) exceeds certain thresholds, you may pay an additional surcharge on top of your Part D premium. In 2025, those surcharges range from $13.70 to $85.50.

You can request reconsideration if your income drops due to life events (e.g., retirement) using form SSA-44.

5. Drug Pricing Negotiations & Manufacturer Penalties

Under the Inflation Reduction Act (IRA), Medicare is now authorized to negotiate prices for certain high-cost drugs, and drug manufacturers must pay rebates if prices rise faster than inflation.

Additionally, as of 2025, manufacturers must pay penalties for unjustified price increases.

Future rounds of drug negotiation are planned, impacting both Part D and Part B drugs by 2028.

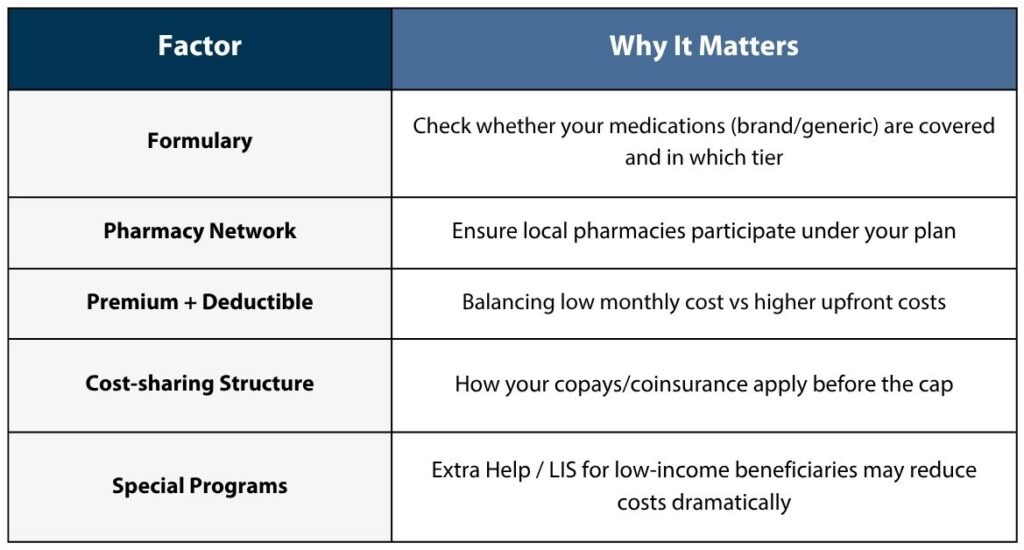

Choosing a Prescription Drug Plan

Plan Types

Standalone Prescription Drug Plans (PDPs): Add-on drug coverage for those with Original Medicare or certain Medicare Cost Plans.

Medicare Advantage Plans with Drug Coverage (MA-PD): These combine Parts A, B, and D under one plan (HMO, PPO, etc.).

Low-Income Subsidy (LIS / “Extra Help”)

If your income and asset limits qualify, you may receive Extra Help, which reduces or eliminates premiums, deductibles, and cost-sharing. Those enrolled in LIS often are automatically assigned to a benchmark (often $0 premium) plan.

Enrollment, Deadlines & Penalties

Initial Enrollment Period (IEP): You have 7 months around your 65th birthday (3 months before, your birth month, and 3 months after) to enroll without penalty.

Annual Enrollment Period (AEP): October 15 – December 7 each year to switch or enroll in a Part D plan for the coming year.

Late Enrollment Penalty: If you go more than 63 days without “creditable drug coverage,” you incur a permanent premium penalty. It’s calculated as 1% of the national base beneficiary premium (for 2025 that base is $36.78) multiplied by the number of uncovered months.

Key Changes Effective in 2025 (and What’s Ahead)

$2,000 out-of-pocket cap on Part D prescription drugs (rather than paying indefinitely).

Simplified benefit structure (three stages vs. gap).

Negotiated drug prices & manufacturer penalties under IRA.

Premiums declined on average for 2025.

Why It’s Important to Enroll Early

Delaying enrollment can cost you permanently due to the late enrollment penalty. Also, your prescription drug costs may rise substantially without coverage, especially if you have chronic conditions or high-cost medications. And with the new out-of-pocket cap, you now have a safety net for expensive drugs — but only if you are enrolled.

How We Can Help You

At MedicareMall, we evaluate your unique medical and prescription needs to help you pick the best Part D plan or Medicare Advantage plan. We also assist with Medigap (supplemental) options. Contact us today and we’ll guide you through:

Comparing plans based on your prescriptions

Avoiding penalties

Enrolling during the right windows

Handling income-based adjustments (IRMAA)

Let me know if you want a version tailored for SEO keywords (e.g. “best Part D plans 2025,” “Medicare drug coverage cap”) or broken into shorter web sections.