Why Medicare Supplement Plan N Is Gaining Popularity in 2025

Medicare Supplement Plan N has quietly become one of the most sought-after Medigap options in recent years—and for good reason. Offering a smart balance between cost and coverage, Plan N is a popular choice among budget-conscious Medicare beneficiaries who still want solid protection.

In this post, we’ll explore why Plan N is rising in popularity, who it’s best for, and how it stacks up against similar plans like Plan G.

Plan N’s Rise in Popularity: What the Numbers Show

- Plan N is now the third most popular Medigap plan, covering about 10% of all Medigap enrollees—roughly 1.4 million people.

- Among newly eligible 65-year-olds, Plan N ranked as the second most chosen plan in 2020, trailing only Plan G.

- Plan N is especially attractive to younger Medicare beneficiaries seeking affordability without sacrificing essential benefits.

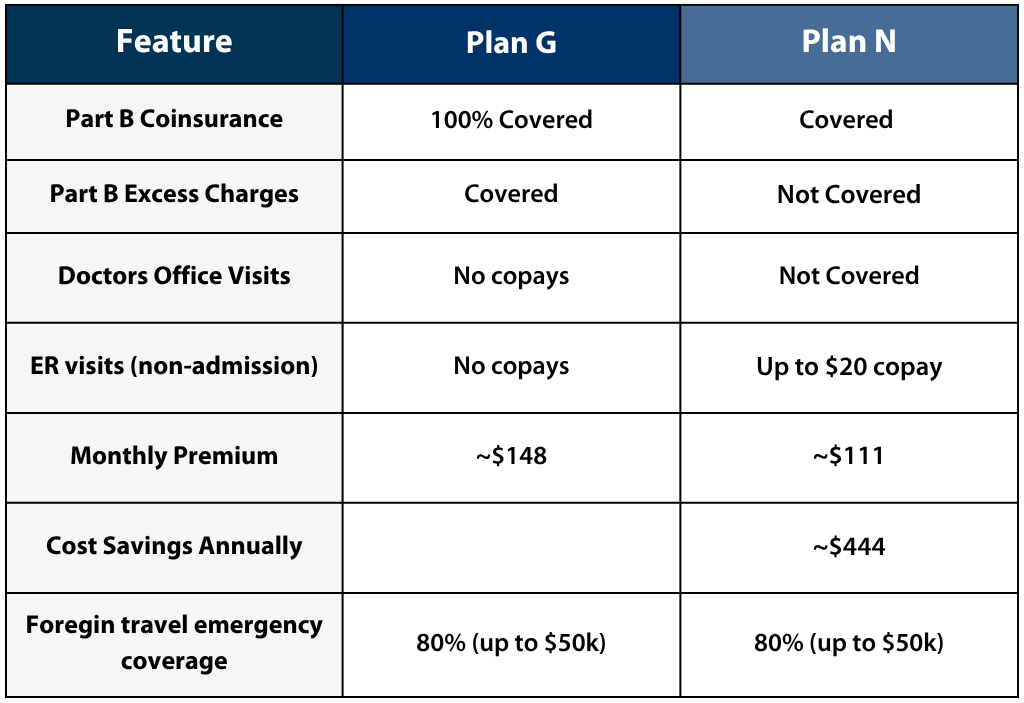

Why Plan N Is Gaining Ground

1. Lower Monthly Premiums

Compared to Plan G, Plan N typically costs 25–30% less. For example:

- Average monthly premium for Plan G (2024): ~$148

Average monthly premium for Plan N (2024): ~$111

This translates to annual savings of around $444, making it a compelling option for those with low to moderate health care usage.

2. Minimal Out-of-Pocket Costs

Plan N requires a few predictable copays:

- Up to $20 for doctor’s office visits (Official Medicare Explanation Here)

- Up to $50 for emergency room visits (if not admitted)

Unlike coinsurance (a percentage of the bill), these fixed copays offer more cost predictability and transparency.

3. Nearly Identical Coverage to Plan G

Plan N covers:

- 100% of Medicare Part A coinsurance and hospital costs

- Skilled nursing facility coinsurance

- Blood (first 3 pints)

- Foreign travel emergency care (80%, up to $50,000)

The only gaps compared to Plan G:

- Part B excess charges (not covered). Check your provider here

- The aforementioned copays

But excess charges are banned in several states (like New York, Connecticut, and Ohio), meaning this isn’t a concern for many enrollees.

4. Healthier Risk Pool = More Stable Premiums

Because Plan N is not guaranteed issue in many cases (outside your initial Medigap enrollment period), it attracts a generally healthier pool of enrollees. This has led to:

- More stable premiums over time

- Less risk of large year-over-year price increases

Who Should Consider Plan N?

Plan N is ideal for:

- Medicare beneficiaries in good overall health

- Those who want lower monthly premiums without sacrificing key benefits

- People who rarely visit the doctor or the emergency room

Residents in states that ban excess charges

Final Thoughts: Is Plan N Worth It in 2025?

For many Medicare beneficiaries, yes—Plan N is absolutely worth it in 2025.

If you:

- Visit the doctor occasionally

- Want premium savings over bells and whistles

- Live in a state that limits excess charges

…then Plan N could be the best value for your money.

However, if you prefer peace of mind knowing you won’t pay copays at all, Plan G may still be the better option—especially for high-frequency users.