Medicare Late Enrollment Penalties: What They Are and How to Avoid Them

If you are new to Medicare, one of the most important things you need to understand is the late enrollment penalty. Missing your enrollment window can result in permanently higher monthly premiums that follow you for the rest of your time on Medicare. These penalties are not a one-time fine. They are added to your bill every single month, and for most parts of Medicare, they never go away.

This page explains what Medicare late enrollment penalties are, when they apply, how much they cost, and the steps you can take to avoid them entirely.

What Is a Medicare Late Enrollment Penalty?

A Medicare late enrollment penalty is an extra amount added to your monthly Medicare premium when you do not sign up for Medicare when you are first eligible and you do not have qualifying coverage that excuses the delay. The penalty is calculated based on how long you went without coverage, and in most cases it is added permanently to your premium.

Late enrollment penalties can apply to Medicare Part A, Part B, and Part D. They do not apply to Medicare Advantage (Part C), though you must still be enrolled in Parts A and B before joining a Medicare Advantage plan.

Your Enrollment Window: The Initial Enrollment Period (IEP)

Most people first become eligible for Medicare at age 65. When that happens, you have a seven-month window called the Initial Enrollment Period (IEP) to sign up. This window opens three months before the month you turn 65, includes your birthday month, and closes three months after your birthday month.

Signing up during your IEP is the simplest way to avoid a late enrollment penalty. If you enroll in the three months after your birthday month, be aware that your coverage start date may be delayed by one to three months, which could temporarily leave you without coverage. Enrolling in the first four months of your IEP ensures your coverage begins on time.

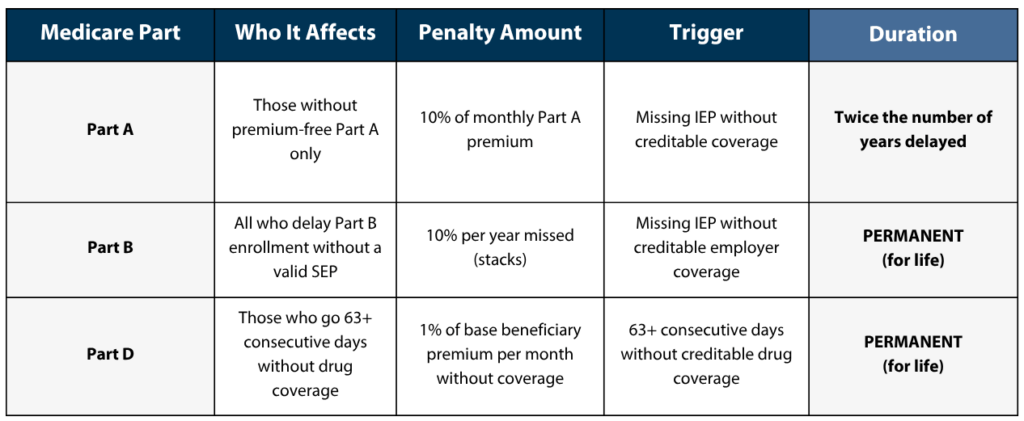

Medicare Part A Late Enrollment Penalty

Who Is Affected?

Most people do not face a Part A late enrollment penalty because most people qualify for premium-free Part A. If you or your spouse paid Medicare payroll taxes for at least 10 years (40 work quarters), you receive Part A at no cost and no penalty applies for late enrollment.

The Part A late enrollment penalty only affects people who do not qualify for premium-free Part A and need to purchase it. In 2026, the monthly premium for purchased Part A is:

- $311 per month if you have 30 to 39 work quarters

- $565 per month if you have fewer than 30 work quarters

How Much Is the Part A Penalty?

If you have to pay for Part A and you miss your IEP without having creditable health coverage, your monthly premium increases by 10%. That 10% is applied to whatever your Part A premium is at the time.

How Long Does the Part A Penalty Last?

Unlike the Part B and Part D penalties, the Part A late enrollment penalty is not permanent. You pay it for twice the number of years you delayed enrollment. For example, if you were eligible for Part A but waited two years to enroll, you pay the 10% penalty for four years before it is removed.

Medicare Part B Late Enrollment Penalty

The Part B late enrollment penalty is one of the most important to understand because it is permanent and it compounds the longer you wait.

How Much Is the Part B Penalty?

For every full 12-month period that you could have had Part B but did not sign up, your monthly Part B premium increases by 10%. These increases stack. Two years late means a 20% penalty. Five years late means a 50% penalty. The 2026 standard Part B premium is $202.90 per month.

How Long Does the Part B Penalty Last?

The Part B late enrollment penalty is permanent. You pay it every month for as long as you have Medicare Part B. As the standard Part B premium rises each year, the dollar amount of your penalty will also increase because it is calculated as a percentage of the current premium.

Medicare Part D Late Enrollment Penalty

Medicare Part D covers prescription drugs. If you go 63 or more consecutive days without Medicare drug coverage or other creditable prescription drug coverage after your IEP ends, you will face a Part D late enrollment penalty when you eventually enroll.

How Much Is the Part D Penalty?

The Part D penalty is calculated differently from Part A and Part B. Instead of being based on a fixed percentage per year, it is based on the national base beneficiary premium, which Medicare sets annually. The penalty is 1% of that base premium for each full month you went without qualifying drug coverage.

In 2026, the national base beneficiary premium is $38.99 per month. This means each month you go without coverage adds approximately $0.39 to your future monthly premium, permanently.

How Long Does the Part D Penalty Last?

The Part D late enrollment penalty is permanent. It stays with you for as long as you have any Medicare prescription drug coverage, even if you switch Part D plans.

How to Avoid Medicare Late Enrollment Penalties

1. Enroll During Your Initial Enrollment Period

The most straightforward way to avoid every Medicare late enrollment penalty is to sign up during your seven-month Initial Enrollment Period. If you are receiving Social Security benefits when you turn 65, you are usually enrolled in Parts A and B automatically. If you are not receiving Social Security, you need to actively sign up through the Social Security Administration online, by phone, or at your local Social Security office.

2. Maintain Creditable Coverage

If you are still working at 65 and have health insurance through your employer or your spouse’s employer, you may delay Medicare enrollment without triggering a penalty, provided that coverage meets Medicare’s standards. This is called creditable coverage. Once that employment-based coverage ends, you must act promptly to enroll.

Coverage from COBRA, retiree health plans, or individual marketplace plans does not count as creditable coverage for purposes of avoiding the Part B late enrollment penalty. Do not assume that any prior insurance coverage protects you from a penalty. Confirm with your benefits administrator or a licensed Medicare agent.

3. Use a Special Enrollment Period (SEP)

If you delayed Medicare because you had qualifying employer coverage, you are entitled to a Special Enrollment Period when that coverage ends. This gives you a penalty-free window to sign up:

- Part A and Part B: You have 8 months to enroll after your employer coverage ends or your employment ends, whichever comes first.

- Part D: You have 63 days to enroll in prescription drug coverage after your creditable drug coverage ends.

Do not wait until the end of those windows. Enroll as soon as possible after your employer coverage ends to avoid any gap in coverage or an accidental penalty.

What Counts as Creditable Coverage?

Creditable coverage means health or drug insurance that provides benefits at least as valuable as what Medicare covers.

For Part B (Medical Coverage):

- Group health insurance through an active employer with 20 or more employees

- Coverage through a spouse’s active employer meeting the same standard

Coverage that does NOT count for avoiding the Part B penalty includes COBRA continuation coverage, retiree health plans, and individual marketplace plans. Even if an employer contributed to that coverage, if you are no longer actively employed, it does not protect you from the Part B penalty.

For Part D (Prescription Drug Coverage):

- Employer-sponsored or union drug plans that pay at least as much as the standard Part D plan on average

- Veterans Administration (VA) drug coverage

- TRICARE drug coverage

- Federal Employees Health Benefits (FEHB) drug coverage

Employers and unions are required by law to notify Medicare-eligible employees each year about whether their drug coverage is creditable or non-creditable. If you receive a notice stating that your drug coverage is non-creditable, you should enroll in a Part D plan immediately to avoid accumulating a penalty.

What If You Miss Your Initial Enrollment Period?

If you miss your IEP and do not qualify for a Special Enrollment Period, you still have another option: the General Enrollment Period (GEP). This runs annually from January 1 through March 31, with coverage beginning July 1 of that year. However, enrolling during the GEP does not protect you from late enrollment penalties. You will still owe a penalty for the time you went without coverage.

If you missed your IEP and are unsure whether you qualify for a Special Enrollment Period or whether you owe a penalty, speaking with a licensed Medicare agent before you enroll is the best course of action.

Frequently Asked Questions

Are Medicare late enrollment penalties a one-time fee? No. Late enrollment penalties are added to your monthly premium and charged every month for as long as you have that type of Medicare coverage. For Parts B and D, that means the penalty lasts the rest of your life.

Can a Medicare late enrollment penalty be waived or appealed? In most cases, no. Penalties are waived only in rare situations, such as when you received incorrect official information from the Social Security Administration or Medicare that directly caused you to miss your enrollment window. The burden of proof falls on you, and approvals are uncommon. Prevention is far more effective than appealing after the fact.

Does Medicare Advantage (Part C) have a late enrollment penalty? There is no separate late enrollment penalty for Medicare Advantage. However, you must be enrolled in Medicare Parts A and B to join a Medicare Advantage plan. If you delayed Part B and owe a penalty, that penalty remains even if you later enroll in Medicare Advantage.

I am still working at 65. Do I need to sign up for Medicare? It depends on the size of your employer. If your employer has 20 or more employees, you can delay Medicare without penalty as long as you remain on that employer’s group health plan. If your employer has fewer than 20 employees, Medicare would likely be your primary insurance and you should enroll to avoid a penalty and gaps in coverage. Confirm your situation with your HR department or a licensed Medicare agent before making any decision.

What if I was enrolled in Medicaid or a Medicare Savings Program? Certain low-income assistance programs, including the Part D Low Income Subsidy (also known as Extra Help), eliminate or reduce the Part D late enrollment penalty. If you qualify for Extra Help, you will not be charged a Part D penalty. You should still enroll in Medicare Parts A and B on time to avoid those separate penalties.

Does the penalty amount stay the same every year? For Part B, the dollar amount of your penalty will change each year because it is calculated as a percentage of the current standard premium, which changes annually. The percentage itself stays fixed, but as premiums rise, so does what you owe. The Part D penalty works similarly, as it is based on the national base beneficiary premium, which also changes each year.